In this piece

Journalism, media, and technology trends and predictions 2025

A person holds their phone showing social media applications. Reuters / Asanka Brendon Ratnayake

In this piece

Executive summary | 1. Journalism embattled but unbowed | 2. Disruption of search poses existential challenge | 3. Wider platform uncertainties create new dilemmas | 4. Driving business growth through product innovation | 5. Personalities, influencers, and the ‘Creator-fication’ of news | 6. Managing and retaining talent in the newsroom | 7. Combating news fatigue amongst journalists and audiences | 8. Generative AI and newsroom transformation | 9. Intelligent agents and conversational interfaces: the next big thing? | Conclusion | Survey methodology | Footnotes | About the authors | AcknowledgementsDOI: 10.60625/risj-vte1-x706

Executive summary

News organisations are braced for multiple challenges in 2025 that will likely include further attacks from hostile politicians, continued economic headwinds, and battles to protect intellectual property in the face of rapacious AI-driven platforms. Changes to search, in particular, will become a major grievance for a news industry that has already lost social traffic and fears a further decline in visibility as AI interfaces start to generate ‘story like’ answers to news queries. The US election also highlighted the growing power of an alternative news ecosystem that includes partisan personalities and creators that often operate outside journalistic norms, and some say have now eclipsed the mainstream media in terms of both influence and trust.

Despite these difficulties many traditional news organisations remain optimistic about the year ahead – if not about journalism itself. Uncertain times tend to be good for business and the prospect of ‘Trump unleashed’1 could lead to a surge in web traffic and even in subscriptions. But this is by no means guaranteed. One key challenge will be to re-engage audiences that have fallen out of the habit of consuming news over recent years and to find ways of attracting the next generation. Many publishers will be looking to dramatically upscale the quality of their own websites, create more personalised news experiences, and invest further in audio and video. With consumer expectations moving at a rapid pace, embracing change while staying true to core journalistic values will be the key balancing trick for the year ahead.

How media leaders view the year ahead

These are the main findings from our industry survey, drawn from a strategic sample of 326 digital leaders from 51 countries and territories.

- Just four in ten (41%) of our sample of editors, CEOs, and digital executives say they are confident about the prospects for journalism in the year ahead, with one in six (17%) expressing low confidence. Stated concerns relate to political polarisation, a rise in attacks on the press, and media capture – all of which in combination are seen as significant threats to journalism’s ability to operate freely.

- More positively, just over half (56%) say they are confident about their own business prospects, a significant jump on last year’s figure. Many publishers expect traffic boosts amid the expected chaos of a second Trump presidency, others report continuing growth in online subscriptions, while others still think that the rapid growth of unreliable AI-generated content could bring audiences back to trusted media.

- Meanwhile, around three-quarters (74%) of our survey respondents say they are worried about a potential decline in referral traffic from search engines this year. Data sourced for this report from analytics provider Chartbeat shows that aggregate traffic to hundreds of news sites from Google search remains stable for now but publishers fear the extension of AI-generated summaries to important news stories. This comes after big falls in referral traffic to news sites from Facebook (67%) and Twitter (50%) over the last two years.2

- In response to these trends, publishers will be putting more effort this year into building relationships with AI platforms (+56 net score3) such as ChatGPT and Perplexity, both of which have been courting high-quality content in return for citations and/or money. With consumer attention switching to video, more publisher effort is also being planned for YouTube (+52) and TikTok (+48) – despite a possible ban in the United States early in 2025 – as well as Instagram (+43).

- By contrast, publisher sentiment towards X/Twitter (-68 net score) has worsened this year following the politicisation of the network under Elon Musk. The Guardian, Dagens Nyheter, and La Vanguardia are amongst those to have stopped posting on the platform, with Bluesky (+38) a key beneficiary. Google Discover (+27) is becoming a more important – if volatile – traffic source that has become critical to many news businesses over the last year. Our survey finds publishers ambivalent but also realistic about their dependence on platforms overall, with a similar proportion looking to cut ties (31%) as strengthen them (31%). Most of the rest (36%), are planning to maintain ties at existing levels.

- On the business side, almost four in ten (36%) of our commercial publishers expect licensing income from tech and AI companies to be a significant revenue stream – twice as many as last year. But the amount and structure of any deals remain a point of contention. The majority of our survey respondents (72%) said they would prefer to see collective deals that benefited the whole industry rather than each company negotiating in their self-interest (19%), which is mostly what has been happening. A further 6% say they would rather not enter into any deals.

- More widely, subscription and membership remain the biggest revenue focus (77%) for publishers, ahead of both display (69%) and native advertising (59%). The majority are now relying on three or four different revenue streams, including events (48%), affiliate revenue (29%), donations (19%), and related businesses (15%).

- With subscription growth slowing, new product development is set to be a more important priority in the year ahead. More than a quarter of our publisher respondents say they are actively thinking about or planning to launch new products around games (29%) or education (26%) with one-fifth (20%) looking to launch an international or foreign language version. Many of these new products are likely to be bundled into ‘all-access’ subscriptions in a bid to reduce churn. At the same time more than four in ten (42%) say they’ll be looking to launch or trial a ‘youth’ product this year.

- Meanwhile news organisations’ use of AI technologies continues to increase across all categories, with back-end automation (60%) considered very important by publisher respondents, many of whom have rolled out AI toolkits to support new workflows this year. The vast majority (87%) say that newsrooms are being fully or somewhat transformed by Gen AI, with just 13% saying not so much or not at all.

- Audience-facing uses of AI are likely to proliferate in 2025 with publishers leaning into format personalisation as a way of increasing engagement. In our survey the majority said they would be actively exploring features that turn text articles into audio (75%), provide AI summaries at the top of stories (70%), or translate news articles into different languages (65%). Over half (56%) of respondents said they would be looking into AI chatbots and search interfaces. Not all these experiments will make it into full production but the direction of travel is clear.

- More widely, respondents expect to see tech platforms developing and promoting their AI agents this year – many coming with improved conversational interfaces. OpenAI’s ChatGPT now comes with advanced voice features and both Siri and Alexa are getting an upgrade. Around one-fifth (20%) think these interfaces will be the ‘next big thing’, with half (51%) expecting more of a ‘slow burn’ impact.

- Publishers are in two minds about whether the trends towards influencers and creators is good or bad for journalism. Around a quarter (27%) take a negative view, worrying that institutional news reporting could get squeezed out, but others (28%) are more positive, feeling that there is much that news organisations can learn in terms of storytelling creativity and building communities.

- Linked to the above, some publishers worry about losing their editorial stars in a more personality-led ecosystem. But a bigger concern is around attracting and retaining talent in product and design (38%), data-science (52%), and engineering (55%) at a time when new product development is becoming more important than ever.

Words and phrases we could be hearing more of in 2025…

AI Slop

AI Slop[/ ai slɔp /’] noun

[/əˈd͡ʒɛn.tɪk/] adjective

Def: Able to express agency on one’s own behalf or that of another. Will increasingly be used this year in the context of Gen AI agents that exercise control by anticipating our needs.

[/ˈbrein rɔt /] noun

Def: Supposed deterioration of a person’s mental or intellectual state, as the result of overconsumption of material (esp. online) considered to be trivial or unchallenging. Oxford University Press word of 2024.

[/influɛncɛr’] noun

Def: A person who is able to influence consumption, lifestyle or political preferences of online audiences by creating engaging content on social media. Often used disparagingly by journalists in the context of news.

The remainder of this report is divided into nine themes or chapters with a discussion of each followed by some more specific predictions about what might happen in 2025.

Our podcast with the authors

Spotify | Apple | Transcript | Also listen to an AI generated podcast on the report made using NotebookLM.

1. Journalism embattled but unbowed

While many publishers have confidence in their own news organisations, this year’s survey shows an alarming decline in confidence in journalism in just a few short years. Only four in ten (41%) say they are confident, down 19pp from the figure in our 2022 poll. The proportion that says they are not confident has risen from 10% to 17% over the same period.

It’s not difficult to see why this is happening. Across the world – and especially in societies that have become increasingly polarised – prominent politicians have been attacking or looking to undermine independent journalists, scrutinising their actions with threats, lawsuits, or worse. In a growing number of countries existing or new legislation, including national-security type laws, is being used to make it harder or more dangerous for journalists to operate.

But it is not just direct attacks. Politicians are increasingly finding ways to bypass the media entirely. In the recent US election, the two main candidates Donald Trump and Kamala Harris largely avoided mainstream news outlets, preferring to use their own channels or talk with alternative sources such as podcasters or YouTubers. In Trump’s case, key messages were then amplified by a network of social media outriders.4 ‘The Trump victory has confirmed the media influence in the public is deteriorating rapidly, even more than we thought,’ says Emilio Doménech, CEO of Watif in Spain.

These tactics have proved particularly effective at engaging those who rarely access (and have low trust in) the established media – and not just in the United States. Calin Georgescu rose from near obscurity to top the poll in the first round of the Romanian presidential election, fuelled by a combination of populist, anti-establishment rhetoric and a hugely successful social media campaign, principally via TikTok.5 His account showed him horse riding, vigorously exercising, and attending church, and he largely avoided media set pieces such as TV debates. Accusations of foreign (Russian) interference means that the elections will now be rerun but it is far from clear that the result was not a reflection of the popular mood.

Of course, the undermining of the news media doesn’t just come from politicians: ‘You are the media now’, said Elon Musk, suggesting that posts on his social media platform are now as credible as content from traditional news outlets. With mainstream media hampered by low trust and difficult economics, this chorus of criticism could prove hard to counter this year.

Around 2,500 jobs were lost in 2024 in major markets according to Press Gazette, following around 8,000 the previous year. The Wall Street Journal, the Guardian, Daily Mail, Vox, Axios, and the Daily Maverick are just some of the brands affected.

Television news faces a year of downsizing around the world as audience attention shifts to streaming platforms. In the United States CNN is braced for hundreds of layoffs and has lost around a third of its audience since the election. Public broadcasters are also struggling to attract audiences for traditional news shows and many also face attacks from mostly right-wing politicians and ‘defund’ pressure groups. In Switzerland public broadcaster SRG SSR is facing another referendum which threatens to cuts its funding in half. The BBC is amongst those to have cut staff and key news programmes in 2024.

Despite this, over half of our survey respondents (56%), many of whom represent richer subscription-based publishers in Northern Europe or the United States, remain confident about their business prospects despite the tough economic and political outlook.

Sentiment amongst publishers, overall, remains defiant, with a strong belief that at times of uncertainty independent journalism will be more important than ever. Persuading audiences of that in an increasingly hostile and polarised environment will be the key challenge for the year ahead.

What may happen this year

- Trump steps up attacks on the news media: Donald Trump has threatened to cancel broadcast licences of TV networks over ‘unfair’ coverage and to jail journalists who refuse to reveal sources. These threats may not be carried out, but the rhetoric could have a chilling effect on media coverage. Trump is likely to restrict access for mainstream journalists, potentially even in the White House briefing room, and cosy up further to supportive ‘alternative’ media. Federal funding to public broadcasters will be likely be cut along with that for non-profits engaged in fact-checking, which Trump considers to be censorship.

- News media get less confrontational: Expect to see a different approach this time round, with less media outrage about Trump’s lies and more coverage of the impact of his policies. The non-endorsement of Kamala Harris by the Washington Post may also be a sign that some owners may not be willing to put their wider commercial interests in the firing line over the next four years, despite a wave of cancellations from digital subscribers and the resignation of prominent columnists.6

- Trump playbook replayed elsewhere: Populist politicians around the world have taken note and are busy building and incentivising alternative networks to amplify their messages through digital channels. Expect claims of foreign interference (as in Romania, Germany) to become an increasing focus for security services, with more pressure on platforms at election time.

2. Disruption of search poses existential challenge

In last year’s report we showed how referral traffic to publishers from Facebook had collapsed as the network pulled back from news and invested instead in more ‘joyful’ creator content. Traffic from X also fell significantly as Elon Musk made the network less publisher-friendly. But now publishers are worried that search traffic may be next to fall as the big players integrate AI-generated summaries that could further reduce exposure to news links.

Data from the analytics company Chartbeat from almost 2,000 news sites, sourced for this report, give a good overview of the impact of platform changes. Aggregate Facebook traffic to news and media properties has declined by two-thirds (67%) in the last two years and traffic from X is down by a half (50%). However, there does not yet appear to be any decline in aggregate traffic from Google Search, despite reports to the contrary by some individual publishers.7 At the same time, Google Discover, a set of personalised news links that are shown via the Chrome browser on mobile devices and via the Google app, has grown significantly over the last year (+12%) and delivers more combined traffic than organic search.

Google was initially cautious in its rollout of its ‘AI overview’ feature (real-time answers to specific questions) after an early version suggested using non-toxic glue to make cheese stick to pizza. So far, queries around important news stories have been largely excluded but publishers worry that this will change, turning multiple blue traffic-generating links into a smaller number of ‘citations’. Google argues that links within AI overviews deliver more click-throughs than in a traditional web listing, though there may be fewer links visible overall. But new competition is on the way in the form of OpenAI’s Search GPT and Perplexity. These AI disrupters will feel less constrained than Google as they combine the power of foundational LLMs (Large Language Models) with real-time indexes of information to significantly improve the search experience.

ChatGPT Search, launched at the end of 2024, gives a sense of where the new landscape may be headed. It draws its results from a range of sources with whom OpenAI has been doing deals. These include a licensing arrangement reportedly worth around $250m over five years with News Corp, which owns brands such as the Wall Street Journal, the New York Post, The Times, and the Sun.8 Reuters, the AP, Financial Times, and Le Monde have also agreed significant deals. In this example a query about Syria brings back not a ‘snippet’ but an aggregated story with citations at the end of each paragraph.

Towards the bottom of the article, there is a box containing more conventional blue links. In this arrangement, publishers that have signed deals get preferential treatment. At the same time, the platform (OpenAI) benefits from credible information that has been checked by journalists.

OpenAI’s approach to try to do deals with a small number of premium publishers is being mirrored by Apple and Amazon (for its Alexa platform). By contrast, Google has so far chosen not to pay specifically for AI overviews, while X has updated its terms of service to allow content posted to its platform to be used without explicit consent or compensation. Other key players such as Perplexity and ProRata, which will be launching its own search engine Gist.ai in early 2025, are offering revenue share options for publishers.

But these new-style aggregations are not going to stop with search queries. Perplexity recently added a ‘For You’ page, a constantly updating personalised news service. An automated elections results hub was created for the US elections that was hard to distinguish from those on the websites of major news sites.

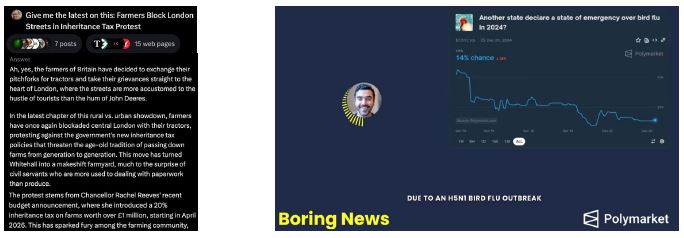

Particle is a mobile app that offers real-time summaries of multiple stories in a personalised interface. Links to the originating stories are shown, but below the fold. Grok Stories, now available for free on X, is another automated news service drawn from a combination of user-generated and mainstream media posts. And Boring News takes its inspiration from the Polymarket betting odds, which did a better job of predicting the US election result than most opinion polls, and creates an automated daily audio round up of stories that could affect the markets.

All these automated news services raise existential questions for journalists and news publishers about their role in this new ecosystem. If people can access summaries of the best content for free, why would they click on to publisher websites. Will any money offered by platforms last? And will it compensate for the loss of traffic?

Then there is the issue of equity. In our survey almost three-quarters of publisher respondents (72%) said they would prefer to see collective deals that benefited everybody, but that is the opposite of what is currently happening – namely a few side deals with international news agencies and national publishers. However, this strong preference for collective agreements in the data may simply reflect the fact that the majority of publishers in our survey do not currently have deals and do not feel they are likely to be offered one any time soon.

Rasmus Kleis Nielsen in his Nieman Lab prediction article shows how early deals have favoured large English-language publishers and suggests that there is ‘zero transparency’ about their nature and value.9 ‘Collective agreements based on nationally or internationally established press organisations should set the proper tone to ensure equitable opportunities for publishers worldwide’, says Tai Nalon, co-founder and executive director of Aos Fatos in Brazil, where platforms have signed contracts with international news agencies while ignoring local companies. ‘This fosters a process of neo-colonialism and erodes vulnerable ecosystems,’ she says.

Others worry that the current approach to deals is already weakening the position of smaller publishers: ‘I believe the rise of generative AI platforms is exacerbating inequalities between large and small publishers and this could worsen their position further as they face a likely decline in search-driven traffic,’ argues José Antonio Navas, Head of Subscriptions at El Confidencial in Spain.

What may happen in 2025?

- Push for government help: Expect renewed calls to force platforms to pay proper compensation for the use of their content. One emerging option is a reworking of so-called ‘news bargaining codes’ that were first introduced in Australia and generated around A$200m from ‘designated platforms’ annually at one stage. After Meta refused to renew its deals, the Australian government is planning to impose a levy on the biggest social and search platforms that needs to be paid whether news content is used or not. This so-called ‘news bargaining incentive’ allows platforms to offset the levy if they do direct deals with publishers.10 Other countries will be watching with interest, though allocating any spoils across multiple publishers with different expectations and objectives could be a fraught process.

- More legal action on the way: Canadian publishers and the New York Times are amongst those seeking damages from OpenAI for using articles without authorisation to train underlying models. The stakes are extremely high if the decision goes against either party, so expect to see this settled out of court or kicked further down the track as negotiations grind on. We can also expect to see cases where publishers (or other plaintiffs) seek compensation or apology for reputational damage. A headline from the BBC was recently reinterpreted by Apple’s new AI systems suggesting, wrongly, that murder suspect Luigi Mangione had shot himself.

- New collaborative intermediaries emerge: ProRata.ai is one of a number of companies, along with Tollbit and Human Native, that are looking to calculate the contribution of a particular article (or publisher) to an AI-generated summary. In this way it offers a mechanism for smaller (and larger) publishers to be paid or at least to help understand its value. The Financial Times, Fortune, Axel Springer, and The Atlantic have all agreed to license their content to ProRata.ai while Danish publishers are partnering in a collective way to ensure the whole ecosystem benefits.11 Expect to see more intermediaries and new products in this space over the next year.

3. Wider platform uncertainties create new dilemmas

In this fast-moving and uncertain environment, publishers remain ambivalent about their relationship with big tech companies, with around a third (31%) wanting to strengthen ties, the same proportion (31%) wanting to cut them, and just over a third (36%) looking to maintain their current position.

‘We are in a marriage of convenience with the platforms,’ says Louise Pettersson, Editor-in-Chief at Sjællandske Medier, a small regional publisher in Denmark. ‘They want to profit from our unique content but refuse to acknowledge us for it, either through traffic or payment. Meta, in particular, is deeply problematic.’ Others see a potential changing of the guard, which offers an opportunity to change the terms of trade in a way that is more advantageous for publishers. ‘It’s a constant reshuffle. While some platforms have stopped caring about factually correct information altogether (X), others stay put and new interesting opportunities (some AI platforms) arise,’ says Matthias Streitz, Head of Editorial Innovation at Der Spiegel.

Our survey shows that building relationships with new AI platforms such as OpenAI and Perplexity will be a key priority this year, with a +56 percentage point difference between those who say they will be putting more effort into AI platforms and those saying they will put less effort into them. Others see opportunities in these emerging gateways to forge a more aligned partnership based on trusted information. ‘[Platforms] know fake news is going to be a big problem long-term, so working closer to us, especially if we can deliver engaging, powerful content, is going to make a difference,’ argues Emilio Doménech from Watif.

There’ll also be a greater focus this year on alternative channels such as WhatsApp (+39), LinkedIn (+39), Bluesky (+38), and Google Discover (+27) – which has become the number one source of referral traffic for many publishers.12

At the same time publisher respondents say they’ll be putting considerably less effort into Facebook (-42 net score), while sentiment towards X (-68) has significantly worsened, with the platform widely viewed as becoming less useful for journalists as well as increasingly toxic for the public. ‘Facebook is becoming increasingly irrelevant to us, and we are deeply relieved that we never became dependent on traffic from Meta,’ notes Gard Steiro, Editor-in-Chief and CEO, VG, Norway. For several years, VG’s main strategy has been to build a destination brand and to prioritise direct relationships. A secondary strategy has been to start to build connections with young people via Snapchat and TikTok.

Video platforms on the rise

The other striking aspect of this chart is the extent to which publishers will be investing more in video networks such as YouTube (+52 net score), TikTok (+48), as well as Instagram (+43), which has also been pushing more short-form video through its algorithms. The 2024 Digital News Report showed how extensive consumption on these platforms has been become, especially with younger audiences, as well as how publishers have been losing out to news creators and influencers in these networks.

But there are many challenges for publishers looking to invest more in this area. Producing video does not come naturally to many print-based newsrooms and short-form video remains hard to monetise, with little opportunity to drive traffic back to websites or apps. An explosion of content in networks like TikTok, including automated and synthetic news, will make it even harder for publisher content to stand out this year.

What may happen in 2025?

- More bans and restrictions on social media: TikTok users in the United States could only have a short time left scrolling through their ‘For You’ pages after a court ruling upholding legislation demanding a TikTok ban unless Chinese parent company ByteDance sells the app to a non-Chinese company. Closing TikTok in the US would be deeply unpopular with millions of users, would deprive creators of one of their main platforms, and have global ramifications. The situation remains fluid, with an appeal to the Supreme Count pending and with incoming president Donald Trump opposed to a ban after it helped him connect with young voters. TikTok is already proscribed in multiple countries, including India, due to concerns about Chinese government influence and potential impact on the young. Elsewhere, expect more legislation aimed at restricting access to networks aimed at the youngest groups, following the social media ban for under-16s in Australia. Elon Musk’s X could also face more fines or bans13 over its reluctance to take down or properly moderate content. We can expect more tension with Europe after recent controversial statements by Musk about German and UK politics raised concerns about interference in domestic affairs.

- Social video explosion: With audiences increasingly appreciating bitesize formats, expect to see more publishers bringing this content into their own websites and apps. The Economist and the BBC are amongst those to have built video carousels into their homepages, while others are embedding vertical videos within stories or commissioning reporter stand-ups for the website in what media commentator Charlie Warzel has termed ‘prestige TikToks’.14

- Bluesky wins over journalists but not the wider public: The X/Twitter clone more than doubled the number of its registered accounts between the middle of September (9 million) and the end of November 2024 (20 million). Many of the new sign-ups were part of an ‘X-odus’ of Democrat supporters, upset by what they see as Elon Musk’s partisan stewardship as well as those worried about misinformation and extremism on the platform.15 News organisations including the New York Times and Financial Times have also been quick to adopt Bluesky, which offers stronger moderation than X and some have reported greater engagement on their accounts than with both X and Threads, despite their much larger user bases (611m and 275m respectively). Part of the reason may be the use of starter packs — lists of accounts in a specific area that can be followed with a single click enabling quick onboarding. Despite the hype, Bluesky is very unlikely to replace X in the short term, but expect it to carve out an important niche in a fragmented and increasingly partisan social media landscape.

4. Driving business growth through product innovation

The combination of the end of the mass referral model and expected further disruptions from AI is forcing publishers to radically rethink business models. With content of every type and format becoming more abundant than ever, only publishers that stand out from the crowd in terms of quality, relevance, or connection are likely to succeed. All of this points towards a continued shift towards reader-funded models and away from advertising predicated on scale.

That change has been reflected in our survey for several years, with subscription outstripping advertising as the most important revenue focus for publishers. But as in previous surveys, we find news organisations also looking to diversify, with most pursuing three, four, or even five different revenue streams. The biggest expected shift in focus (+16pp) comes from platform funding, likely due to a combination of expected AI deals, existing revenue sharing, as well as fact-checking contracts. Support from philanthropic funds and foundations is also expected to be a more important source of revenue, reflecting the pressures on independent public-interest journalism and fact-checking in many parts of the world (see chapter 1). The proportion of publisher respondents relying on crowdfunding and donations (19%) has also increased over the last few years.

Other revenue sources mentioned by publishers include related services, such as training and marketing. Merchandise is an important supplementary revenue stream for some smaller publishers and in a number of European countries legacy commercial media rely in part on government subsidies to support local or public interest journalism.

New product development takes centre stage

In this environment, many publishers worry that current strategies of focusing on improving core products will not be enough. This is why nearly half of publisher respondents (44%) in our survey said they considered it more of a priority to develop new products and services as a way of driving growth.

Some of this year’s initiatives are designed to target hard-to-reach audiences, with around four in ten (42%) saying they are thinking about or planning a new product aimed at young people. Between a quarter and a third say they are actively looking at audio (26%) or video (30%) products or services this year. Others are planning to invest in adjacent areas such as games (29%), education (26%), or food (13%). Much of this is inspired by the example of the New York Times which has created a product portfolio that includes games, sport, recipes, and new product reviews, as well as audio. Much of its growth in recent years has come from these lifestyle products and from the all-access bundling strategy which has significantly improved overall retention.

What may happen in 2025?

- More and different kinds of bundling: Many publishers are looking to replicate the New York Times model by developing new products (as per the chart above) that they can put into an all-access subscription. The Guardian launched a cooking app (Feast) and is looking to add product reviews in 2025 while The Times (of London) and the Telegraph offer puzzle-only subscriptions in the UK. In Sweden, Bonnier’s +Allt bundle includes content from more than 70 Swedish local and national titles as well as magazines, while Mediahuis and DPG are following a similar strategy in the Netherlands and Belgium.

Bundles also make sense from a consumer point of view. The number of news subscription offers has exploded in recent years, with substackers and YouTubers now competing for share of wallet with traditional media – leaving overwhelmed consumers looking for more convenient and cost-effective solutions.

This year we can expect more partnerships between companies that are not part of the same publishing group. Subscribers to leading European brands such as Politiken and FAZ have been able to access the New York Times as part of their subscription for a limited duration. Expect to see these deals extended to more publications as a way to reduce churn or differentiate a more expensive product.

But publishers won’t have it all their own way. Platforms are also looking to get in on the act, with Apple+ finding some success in the US, UK, and Canada in attracting an increasingly extensive range of premium content. As Ben Smith points out in his Nieman Lab prediction: ‘If media companies can’t figure out how to be the bundlers, other layers of the ecosystem – telecoms, devices, social platforms – will.’16

- Audio everywhere: More media companies plan to integrate audio (read articles, audio summaries, and podcasts) into their websites and apps this year. But others are looking to launch separate audio products that they hope will drive both revenue and new audiences. Last year The Economist blazed a trail by putting the majority of podcasts behind a paywall (attracting 30,000 subscribers in six months). Die Zeit has launched an audio app with a separate subscription, and the New York Times will be experimenting with an audio-only subscription through third-party platforms. Because podcasts tend to drive loyalty, many Nordic publishers are including podcasts in their all-access subscription packages.

- Print investment as part of a mixed strategy? The loss of referral traffic from search and social is forcing many publishers to look again at a channel that many have written off but still has timeless attributes. ‘People still derive intellectual and aesthetic pleasure from print,’ says editor-in-chief of The Atlantic Jeffrey Goldberg. ‘It doesn’t beep and flash and demand that you do things. It’s there to be read and enjoyed.’17 The magazine is increasing its print frequency from 10 to 12 issues a year, reverting to a monthly schedule for the first time since 2002. The magazine move reinforces the importance of investing in channels that are not so dependent on the whims and algorithms of big tech companies. In a similar vein digital-born Tortoise Media bought the Observer, the world oldest Sunday newspaper, in December 2024 with a long-term commitment to maintaining its future in print and promising an investment of £25m over five years.

5. Personalities, influencers, and the ‘Creator-fication’ of news

In the wake of the US election there has been much talk about the role of influencers and their impact on politics and the media. But this is not just about big names such as Joe Rogan, Logan Paul, and the Nelk Boys. This trend also encompasses a long tail of influencers and personalities who are capturing attention across a vast swathe of news-related subjects, as well as former journalists setting up on their own.

A recent report from the Pew Research Center18 found that around one-in-five (21%) Americans – including a higher share of adults under 30 (37%) – regularly get news from influencers on social media, with much of the content focused on politics. The majority of news influencers (63%) identified by Pew were men. Over half of the top 150 political TikTok accounts in the US were from content creators rather than journalists according to social-media research firm CredoIQ.19

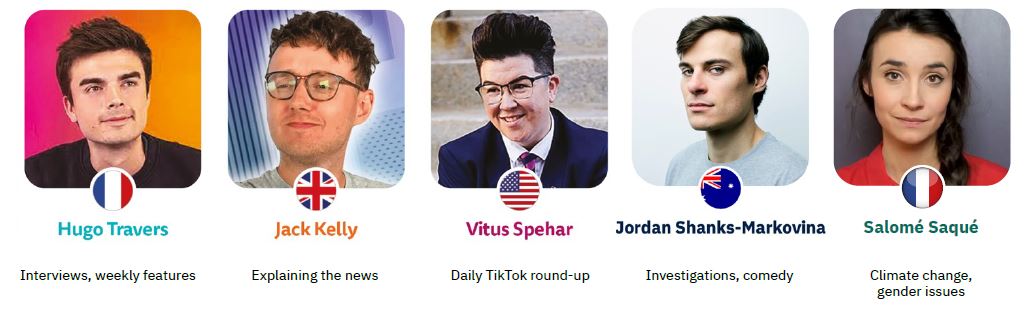

Our own Reuters Institute research from multiple countries documented similar trends. In Brazil prominent social media personalities present a blend of news, entertainment, and opinion via YouTube and Instagram channels. Elsewhere we also found a number of young news creators with a reputation for explaining the news or conducting original investigations. These include Hugo Travers (HugoDécrypte) who has become a ‘go-to’ person for under-30s in France for news, Jack Kelly’s TLDR, Vitus Spehar’s popular TikTok round-up, and Jordan Shanks-Markovina, an Australian YouTuber who blends humour with investigative reporting.

Many of these influencers are providing fresh perspectives or takes on the news, which often feel more authentic than stuffy traditional news formats, even as others have been shown to peddle extreme opinions and conspiracy theories. The Pew study found that the vast majority (77%) of news influencers had no prior journalistic experience, raising questions about the reliability of their content. In a separate report by UNESCO, 62% of surveyed creators said they don’t vet the accuracy of content before sharing it with followers.20

But this picture is further complicated by the exodus from traditional media organisations of a number of prominent journalists who are also leaning into the personality trend. In October 2024, Taylor Lorenz, a technology and internet culture reporter, left the Washington Post to set up ‘User Mag’ Substack and a podcast called Power User. Lorenz, who increasingly identifies with the influencer community, said she wanted autonomy to write, do, and say what she wants without institutional restriction. She also said she prefers a more direct and vocal relationship with her audience, another feature of influencer culture which is often hard to achieve within a traditional media organisation. ‘Legacy media sucks … I’m going to dance on the grave of a lot of these places’, she told the New Yorker.21 These comments illustrate the way in which many influencers position themselves in opposition to mainstream journalism, adding further to the criticism that ordinary people see.

Meanwhile, Tucker Carlson, a former anchor at Fox News, has spent much of the last year building up his ‘alternative’ news brand on various platforms, starting with an exclusive interview with Russian president Vladimir Putin (more than 200m plays on X alone). Other former journalists who have found a home on third-party platforms include Johnny Harris, a former video producer at Vox, who has built a successful YouTube channel around explainer content with more than 6 million subscribers.

The rewards can be considerable. Matthew Yglesias, a co-founder of Vox Media who left for Substack is likely earning over $1m a year from his paid subscribers, according to Business Insider.22

The trend of journalists moving to platforms aligns with the so-called ‘creator-fication’ of journalism, as top talent seeks more control over their content and their audience relationships. Our digital leaders survey reveals mixed views about these trends, with 28% seeing this as positive for journalism and 27% suggesting the opposite.

One senior editor cautions that the focus on personalities could ‘usurp the principles of independent fact-based journalism’, opening the door to ‘yet more opinion, where it is he or she who shouts loudest wins the day’. Others worry about a lack of rigour in checking sources or scrutinising interviewees, creating an even greater problem around mis- and disinformation. ‘I am genuinely concerned about the rise of influencers and other private individuals as more and more citizens turn to them for news and consider them valid agents of information,’ says Daniel Bramon Batlle, from 3Cat in Spain. A recent BBC investigation into Stephen Bartlett’s popular global podcast, Diary of a CEO, found that episodes were increasingly focused on health-related subjects, with over a dozen carrying multiple ‘harmful claims’ that went against extensive scientific evidence.23

But many other respondents to our survey emphasised the positive side in terms of new perspectives, creative storytelling, and a commitment to interact with audiences. ‘We believe that this is a natural evolution in the way audiences consume,’ says Jhulissa Michelle Nogales Cardozo, CEO and founder of the feminist outlet Muy Waso in Bolivia. ‘I believe that many of these content creators have found a new way to relate to communities and have managed to generate something that many media have lost: people’s trust.’

What may happen in 2025?

- Influencer impresarios and umbrella brands: While some creators are happy to work on their own, others are increasingly looking to extend their brand and their business. Johnny Harris works with other creators who share his vision for ‘relatable quality journalism with context and history’ under his New Press publishing company. The latest sign up is Christophe Haubursin, whose Tunnel Vision show investigates topics such as Bitcoin, WhatsApp groups, and the future of fast fashion. Search Party creator Sam Ellis is also part of the network, which creates critical mass in terms of revenue and grows audiences for all the channels. In a different domain Goalhanger is building a network of podcast/vodcast verticals in the UK and US based around well-known personalities who are on a lucrative revenue share for their shows. Much of this talent has been drawn from traditional media companies.

- Media learn to work with influencers: We can also expect to see more tie-ups between traditional media and creators, with both looking to enhance their credibility and reach. Romanian news website PressOne started collaborating with influencers in 2022 to promote news consumption amongst young audiences, followed the next year by a project on drug policy. ‘These collaborations really helped us, at the beginning, to reach the audience that we wanted to reach on Instagram’, says Mălina Gîndu, Social Media Manager at PressOne. In exchange, she says, the influencers benefited from the credibility of being associated with the PressOne brand. As young creators, ‘They were looking to legitimise themselves’, she added. In other cases, media brands have gone a step further hiring creators directly to run social channels on networks like TikTok and Snapchat. This strategy has proved effective for Le Monde in attracting younger audiences, as well as educating them on news literacy in a language and tone they are familiar with.

6. Managing and retaining talent in the newsroom

In an era when audiences, especially younger audiences, tend to pay more attention to individuals than traditional news brands, should newsrooms encourage their journalists to cultivate their own brand personality? Opinions vary. Some, like the head of digital at a European legacy publication, think that ‘if we want to compete … we need to find and create our own influencers’. Mpho Raborife, Managing Editor at News24 in South Africa, believes that ‘there’s still a value in being associated with the brand’ and, while there could be the risk of talent outgrowing the organisation and leaving, this is not yet happening at scale.

Elsewhere, however, the talent exodus has been significant. The BBC has recently lost some of its biggest stars to become podcasters or to go to commercial rivals, most recently one of the Corporation’s highest-profile news journalists Mishal Husain, who has left the flagship Today radio show for Bloomberg.24 Despite this, our survey shows that the vast majority of our respondents (81%) are confident of keeping this top talent, even if they recognise the risks are greater than for other editorial staff.

Digital analytics have made the value of an individual journalist more apparent, showing that editorial stars can often deliver a disproportionate amount of engagement – as well as new subscribers. But managing talent is not without its challenges. ‘I think one of the risks is that, in the end, a few people, especially men, dominate, the image of elDiario.es,’ says María Ramírez, Deputy Managing Editor at elDiario.es, in Spain. The voices of journalists who might be less inclined to show their own face, she says, are in danger of being left behind, potentially leading to unintended gender imbalances.

But the challenges around editorial talent are nothing compared with other parts of the business, as previous Changing Newsrooms reports have shown.25 Over half of respondents say they are not confident about attracting or keeping data scientists (52%) or software engineers (55%). There are also concerns around product and design talent as well as commercial roles. This suggests a significant imbalance, given the need to innovate around new product developments and artificial intelligence. ‘It’s more difficult maybe, to find people [in areas where] there is more competition, because some of these profiles obviously could work for any company that’s not necessarily a newsroom … and usually other industries pay more’, says María Ramírez. ‘But at the same time, if you manage to hire talent in those areas who have an interest and an inclination for news, it’s easier to retain them,’ she added.

What may happen in 2025?;

- More complex negotiations with talent as star power grows: At the end of the day, this is not a new problem. ‘Public radio has always had stars. We have historic examples of people in journalism developing their own brands that become bigger than the brands of the company they represent,’ says Ariel Zirulnick, former Director of News Experimentation at Californian outlet LAist. ‘Network anchors that became the voices of the country in key moments in history. Like Ira Glass, for example.’ But what was different in the past, Zirulnick noted, is that once these stars decided to move on, the transition was managed more gracefully than what seems to be happening now. She added: ‘Yes, these stars’ brands can become bigger than those of their organisations and that makes things more complex for the organisation. You get into questions about retention and special compensation structure and we need to learn how to handle this complexity and how to make it worthwhile for stars to stay. You can’t hold on to those people forever but there are ways to cultivate the next person into a rising star as well.’

- Editorial-tech hybrid newsroom roles become more important: Newsrooms may struggle to hire and retain talent in areas like tech and AI, but it’s an exciting time for editors with an interest in technology. Senior editors such as Jane Barrett at Reuters and Sannuta Raghu at Scroll in India are becoming well-known voices in the AI space using editorial creativity and cultural editorial capital to understand how best to leverage AI for journalistic purposes.

7. Combating news fatigue amongst journalists and audiences

Our research has extensively documented the challenges of combating news fatigue amongst audiences who decide, at times, to disengage and even opt out entirely from a difficult news agenda. Across countries in our most recent Digital News Report, almost four in ten (39%) said they sometimes or often avoid the news.26 The ongoing wars in Gaza and Ukraine, combined with the growing impact of climate change have added to the challenges facing news organisations this year.

How to engage audiences with difficult but important stories, without pushing people away entirely? How to give a sense of hope around conflicts that seem entirely devoid of it? There are no easy answers to these questions, but here are some newsroom strategies.

- The Guardian runs a daily explainer, with key bullet points about the Russia–Ukraine war. ‘It’s consistently popular and with high reading times – and absolutely seems to serve those with a strong interest but who don’t want to follow the exhausting pace of the live blogs and developments’, said Chris Moran, Head of Editorial Innovation.

- Dagens Nyheter in Sweden uses a variety of formats including live blogs, podcasts, and social video. Human stories are a powerful way to show the impact on ordinary lives. One story on TikTok on what happened to a group of friends who were celebrating a bachelor party before the war in Gaza was particularly successful in engaging younger audiences (see illustration on p. 29).

- Helsingin Sanomat showed photographs of the devastation in Gaza to members of the Finnish parliament and wrote a story capturing their feelings and reactions: ‘A change of method can bring the conflict closer and engage a new audience’, says Managing Editor, Product Jussi Pullinen.

It’s not just audiences who are affected by the intensity of covering these conflicts and the criticism that often comes with this. According to recent surveys over half of media workers in countries as diverse as Canada, Spain, and Ecuador reported high levels of anxiety, with one in five reporting depression.27 This amounts to a prolonged mental health crisis that cuts across generations.

What may happen in 2025?

- Pressures move to older generations: Mpho Raborife, Managing Editor at News24 in South Africa, was a Reuters Institute Fellow in 2023: ‘When I was doing my paper with the Institute last year28 I was highlighting the fact that, because of how they experience life on the planet and some of the economic and social stresses, they’re a little bit more prone to anxiety and depression, isolation and even mental health illnesses, but a year later, I can tell you now that this feeling is wider than a younger journalist effect.’ She continued: ‘The older generations have found ways to cope with it or have maybe unhealthy ways of blocking things out and not necessarily addressing them, as opposed to the younger journalists who will ask to tap out earlier than the elder generations do.’ Expect to see high-profile correspondents and war reporters talking more about these issues in 2025.

- Positive news products as part of the mix: Around a third of those that stop their elDiario.es subscriptions say they are fatigued by the news or don’t have enough time.29 In response the publication is looking to introduce a new product offering, maybe a newsletter, that selects just the best or the more interesting news of the month, or, alternatively, news with a constructive or positive angle.

- More signal, less noise: Slow journalism will be back on the agenda this year. Finnish start-up Uusi Juttu (New Thing) is looking to shake up the traditional media when it launches at the start of 2025, with insights and support from the team behind Zetland in Denmark. The team plans to publish just a couple of in-depth features a day with daily audio and newsletter briefings on top. In a similar vein, the Swedish newspaper SvD is finding success with Kompakt (tag line ‘Read less, know more’) which is aimed at moderate news readers who want to spend less time on their screens (see case study below).

8. Generative AI and newsroom transformation

Over the last year, news organisations have been getting their heads around the full implications of Generative AI for journalism and for their businesses. At least in some larger newsrooms, principles and guidelines are largely in place and specialist AI roles have been created, as predicted in last year’s report.

This activity is not confined to the newsroom, with commercial, operational, and product teams also looking to get on board. In our survey, it is clear that the focus still remains on back-end efficiencies, with 96% of publisher respondents saying this will be very important or somewhat important in the year ahead. Using AI to improve personalisation and recommendation comes next (80%), followed by content creation (77%) and newsgathering functions (73%) such as verification, data journalism, and investigations. Coding (67%) and commercial uses (63%) are also considered valuable to publishers.

AI toolkits everywhere

Many large publishers such as the New York Times and Financial Times have invested in cross-functional teams to experiment with the technology and support the newsroom with cultural change.

Early outputs have been promising. AI toolkits pull together a set of useful tasks such as headline suggestions and different kinds of summaries. At JP/Politikens Media Group, a central team has created MAGNA, a tool which can assist with a range of editing tasks from correcting spelling errors to generating drafts from just a few basic facts. The tool is used by three different publications in the group and can adapt the content to the different style guides of each. At Helsingin Sanomat, the AI toolkit is focused more on newsgathering and research. This includes translation, support for data investigations, and creating an automated timeline on any story, trained on trusted content, such as Helsingin Sanomat articles.

AI is also helping to transform investigative and data journalism: ‘AI models are enabling us to work with dispersed sources, creating stories that previously required weeks or even months of effort,’ says Antonio Delgado, co-founder of Datadista in Spain. Similar advances are helping to speed up previously laborious processes around verifying misinformation and disinformation in external platforms: ‘Use of AI tools for fact-checking – especially audio and video – has been very effective for us’, says Ritu Kapur, co-founder and CEO of the Quint in India. Der Spiegel is one of many publishers experimenting with using AI to help fact-check copy – functionality that could eventually be built into the Content Management System (CMS).

These initiatives are building powerful learnings about how to get the best out the technology, but it may take time for these investments to pay off. Hiring specialist AI teams to build and maintain in-house applications can be costly and while journalism can be improved and outputs can be enhanced, it is not clear that significant savings will follow. ‘We are still in an experimentation phase but looking for real-world applications that move the needle’, says Simon Regan-Edwards, Product Director at the Daily Mail.

The majority of respondents to our survey feel that newsrooms are being transformed somewhat (63%) or fully (24%) due to Generative AI, though this may be a reflection of what people see in other newsrooms rather than their own. Just 12% say that there is not so much change – or none at all (1%).

Content transformation the next big thing

As publishers gain more confidence with the technology, expect more focus on audience-facing format transformations this year. Advances in voice technologies have made it possible to transform text articles into audio (in multiple languages or tones) and most publishers (75%) are planning to do more with this functionality this year. Beyond that, AI summaries at the top of articles (70%) are likely to become more widespread, over half (56%) are planning chatbot/AI search functionality for audiences to interact with, with around a third (36%) looking to experiment with turning text stories into video (36%). Again, publishers won’t have it all their own way, with AI-driven browsers such as Dia30 also allowing consumers to summarise, rewrite, and reformat articles to suit their own preferences set to launch this year.

A number of publishers have been experimenting this year with their own chatbots that are trained on their own articles and other trusted sources. Aftonbladet was early out of the gate with an ‘election buddy’ that answered questions about the Swedish elections in June 2024. A lot of manual work was required to check the bots’ answers, but overall 180,000 queries were processed with no known ‘hallucinations’.31 In November, the Washington Post launched an experimental Generative AI tool called ‘Ask the Post AI’, which brings back answers on any topic referenced in news articles published by the paper since 2016. The Financial Times is trialling a similar feature, ‘Ask FT’, for its professional users. These services carry some risk but expect some big publishers to integrate these into site search functions this year to significantly improve access to their archive.

What may happen in 2025?

- Third-party tools get smarter: As fast as the media develop their own tools, the big tech companies are adding compelling new features of their own. Third-party tools like Google’s Notebook LM have surprised many with their accuracy and ease of use for a range of journalist tasks such as summarising transcripts, documents, and data for an investigation. Transcription and translation functionalities are being integrated into a range of free tools and their enterprise versions (Google, Microsoft, Zoom, Dropbox), which has opened up AI technology to smaller publishers at relatively low cost. Third-party chatbots are also now performing well in answering news-related queries on subjects like elections, according to a recent Reuters Institute factsheet,32 raising questions about how much effort publishers should put into their own solutions.

- Specialist workflow tools for the news industry: Existing tools such as Chartbeat are getting a makeover, having already integrated AI-driven headline suggestions. Others are looking to use AI to improve moderation of website comments or make workflows more efficient. OpusClip AI (right) turns long video interviews or footage into viral shorts that can be shared on TikTok, YouTube Shorts, and Reels. It picks out the most likely clips, automatically turns the aspect ratio from horizontal to vertical, adds captions and platform specific effects. Given the fragmentation of platforms, these multi-channel repurposing tools will become more important for publishers this year.

- AI-driven content explosion: The release of OpenAI’s Sora ‘text to video’ generator in December 2024 is set to put new capabilities in the hands of millions of ordinary people. This will lead to a surge of hyper-realistic content that may be hard to distinguish from the real thing.

OpenAI also says it’s put in place safeguards to stop the tool being used for damaging deep fakes such as child sexual abuse. Meanwhile our social feeds are already filling up with synthetic content this year. According to one recent study, over half of longer LinkedIn posts are already AI-generated, though it is often hard to tell the difference between this and genuine corporate speak. Some worry that if ‘AI slop’ (low-quality generated content) spreads too fast, it will start to seep into the training data of foundational LLMs, leading to what is known as model collapse.33 The adoption of metadata standards such as C2PA, that provides transparency about the origin of a piece of content, is likely to be crucial in lowering that risk and allowing algorithms to make better decisions about which content to prioritise.

9. Intelligent agents and conversational interfaces: the next big thing?

One of the most intriguing developments of 2025 is likely to be advances in intelligent agents that can work on your behalf, researching assignments, booking appointments, invoicing clients, and purchasing presents for difficult relatives. At least, that is the vision behind services like Apple Intelligence that also promise to protect your data and privacy in the process. Gartner predicts that by 2028 15% or more of day-to-day work decisions will be taken by autonomous agents.34

But as in the example above, we won’t just be typing instructions to our agents we’ll increasingly be talking to them. Both inputs and outputs of the latest versions of Google’s Gemini, OpenAI’s ChatGPT, and Apple’s upgraded Siri are multi-modal, supporting text, video, audio (and computer code). Amazon’s Alexa will also get an AI makeover this year.

Voice interactions with a variety of devices (phones, headphones, smart speakers, and eyewear) have been growing but until now both latency and the quality of responses have been a barrier to adoption. These problems are being gradually overcome. ChatGPT’s new advanced voice mode, for example, offers more natural conversations that pick up non-verbal cues such as the speed at which you talk and responds with more emotion, something that has been missing so far from synthetic voices. It can also reply in different languages and it will also be possible to get updates on breaking news. All this could increase the pain for publishers with little opportunity to credit content creators or provide click-throughs to websites or apps.

On the other hand, conversational interfaces could offer new ways of making long texts more accessible. The release of Notebook LM’s audio overviews released in September 2024 ‘wowed’ the internet by turning dense articles and documents into podcasts.

From our survey publishers recognise the power of conversational interfaces but the majority (51%) feel that consumer adoption will be a slow burn rather than the next big thing (20%).

What may happen in 2025?

- Chat to an article? Expect more websites to allow you not just to listen to an article but to interrogate it through voice chat (or text). Time magazine showcased this feature on their recent Person of the Year, featuring Donald Trump. Using voice cloning technologies these chats could increasingly be held with a digital version of the real author of the article. Platforms and browsers will also be adding these features as standard.

- People get over-attached to their AI agents: As agents get more life-like, there are concerns that they may become emotionally attached to an unhealthy degree. Some young users of Character AI report becoming so addicted that they can’t do their schoolwork.35 OpenAI suggests that more naturalistic interactions in the latest models could heighten the risk of anthropomorphisation (attributing human like traits to a non-human), potentially ‘reducing their need for human interaction’. Some users have even developed romantic feelings towards their AI companions, leading in one case to a virtual ‘marriage’.36 Meanwhile AI chatbots are being touted by some as an answer to poor mental health and loneliness, with new apps offering synthetic therapists and counsellors.

Conclusion

Institutional journalism faces enormous pressures in the year ahead as technology reshapes the way audiences find and consume information – as well as from populist politicians and others looking to undermine its role in fostering informed democratic debate.

‘You are the media now’, the phrase coined by Elon Musk after the US election, and repeated by many others since – aims to push the narrative that the so-called ‘mainstream media’ are becoming increasingly out-of-touch and irrelevant. The vision behind his Grok.ai is that a combination of ordinary people and advanced technologies can replace many of the functions of journalists in a more immediate and less biased way. At the same time, politicians will increasingly look to bypass media scrutiny, talking directly to supporters or by linking up with ‘trusted’ influencers who are sympathetic to their views (or being paid for their efforts).

Meanwhile Reuters Institute research shows that audiences, especially younger ones, are increasingly drawn to the convenience – and entertainment value – of platforms like YouTube and TikTok and in that context are less likely to have a strong direct connection with specific news brands. As the shift to audio and video consumption accelerates, this is likely to further encourage the rise of ‘personalities’ – increasing the competition for both eyeballs and talent.

In this new environment, publishers worry that their carefully crafted, evidence-based news articles will be harder to access in 2025 as social referrals dry up and traditional search links are at least partly replaced by AI aggregations, often drawn from their own work. Arguments over copyright and fair compensation will rage on throughout the year, with the outcomes having a significant bearing on the shape and size of the news industry that eventually emerges.

Despite these challenges, this report shows that news leaders will be looking to do all they can to turn the tide. Publishers recognise they need to rapidly improve their owned and operated platforms and make their digital products more engaging and relevant for audiences. Embracing AI to personalise content and formats will be a part of that but publishers will also want to emphasise the distinctive (and trusted) nature of their journalism and the original ‘human’ reporting that AI will never be able to replicate. At the same time, they will also be looking to shore up the business side by cutting costs, diversifying revenue streams, and attempting to rebundle news with lifestyle content to increase habit and loyalty.

Not all media companies will be able to adapt fast enough and that will be increasingly evident, but times of change also throw up new opportunities. A big part of the task for news leaders in the year ahead will be to redefine the role and value of journalistic institutions in an age of polarisation, misinformation, and super-abundant content in a way that resonates with both staff and audiences.

Survey methodology

326 people completed a closed survey between 20 November and 20 December 2024. Participants, drawn from 51 countries and territories, were invited because they held senior positions (editorial, commercial, or product) in traditional or digital-born publishing companies and were responsible for aspects of digital or wider media strategy. The results reflect this strategic sample of select industry leaders. Typical job titles included Editor-in-Chief/Executive Editor, CEO, Managing Director, Head of Digital, Director of Product, and Head of Innovation. Just over half of participants were from organisations with a print background (54%), a quarter (25%) came from commercial or public service broadcasters, with around a fifth (18%) from digital-born brands. A further 6% came from B2B companies or news agencies. These proportions are similar to previous surveys.

The 51 countries and territories represented in the survey included Australia, New Zealand, Taiwan, Hong Kong, Singapore, the Philippines, Thailand, Vietnam, Japan, Nigeria, South Africa, Paraguay, Honduras, Uruguay Mexico, Brazil, Colombia, and Israel, but the majority came from the UK, US, or European countries such Germany, Spain, France, Austria, Finland, Norway, Denmark, and the Netherlands as well as Poland, Hungary, and Slovakia, amongst others.

Participants filled out an online survey with specific questions around strategic and digital intent in 2025. Over 90% answered most questions, although response rates to questions vary. The majority contributed comments and ideas in open questions and some of these are quoted with permission in this document.

Footnotes

1 Sewell Chan, ‘Prospects for Journalism in a Second Trump Term’, Nouvelles Pratiques du Journalisme Conference, Sciences Po, Paris, 3 December 2024.

2 Data based on the number of page view referrals in aggregated to hundreds of news websites and apps in the Chartbeat network.

3 Net score is the percentage point difference between the proportion that responded with ‘less effort’ and ‘more effort’.

7 The Sun (News UK) and Immediate Media are amongst publishers to suggest that Google changes have affected its site traffic. The Media Leader

11 The Danish Press Publications’ Collective Management Organisation (DPCMO) has signed a Letter of Intent (LOI) with ProRata.ai to explore collaborative opportunities:

18 Pew defined news influencers as individuals who regularly post about current events and civic issues and have at least 100,000 followers on any of Facebook, Instagram, TikTok, X, or YouTube.

25 See our Changing Newsrooms 2021 report

29 Interview with María Ramírez.

30 AI-centric web browser being developed by The Browser Company, the creators of the Arc browser. Set to launch in early 2025.

About the authors

Nic Newman is Senior Research Associate at the Reuters Institute for the Study of Journalism, where he has been lead author of the annual Digital News Report since 2012. He is also a consultant on digital media, working actively with news companies on product, audience, and business strategies for digital transition. He has produced a media and journalism predictions report for the last 15 years. This is the ninth to be published by the Reuters Institute. Nic was a founding member of the BBC News Website, leading international coverage as World Editor (1997–2001). As Head of Product Development (2001–10) he led digital teams, developing websites, mobile, and interactive TV applications for all BBC Journalism sites.

Federica Cherubini is Director of Leadership Development at the Reuters Institute for the Study of Journalism and an expert on newsroom operations and organisational change, with ten years’ experience spanning major publishers, research institutes and editorial networks around the world. Federica has authored the annual Changing Newsrooms Report (2020–3) and is interested in devising and implementing new and improved ways of working, bridging people, disciplines, departments, projects, and cultures. She is also an expert on newsletter strategies and editorial initiatives that drive audience loyalty.

Acknowledgements

The authors would like to thank the 326 news executives from 51 countries and territories who responded to a survey around the key challenges and opportunities in the year ahead.

Respondents included 65 editors-in-chief, 63 CEOs or managing directors, and 53 heads of digital or innovation, and came from some of the world’s leading traditional media companies as well as digital-born organisations (see breakdown at the end of the report).

Survey input and answers helped guide some of the themes in this report and survey data have been used throughout. Some direct quotes do not carry names or organisations at the request of those contributors.

The authors are particularly grateful to Richard Fletcher, Director of Research, and the wider team at the Reuters Institute for their ideas and suggestions, and to a range of other experts and news executives who generously contributed their time in background interviews (see full list at the end of this report). Thanks also go to Alex Reid for her input on the manuscript over the holiday season and keeping the publication on track. As with many predictions reports there is a significant element of speculation, particularly around specifics and the report should be read bearing this in mind. Having said that, any mistakes – factual or otherwise – should be considered entirely the responsibility of the authors.

Published by the Reuters Institute for the Study of Journalism with the support of the Google News Initiative (GNI).

This report can be reproduced under the Creative Commons licence CC BY.

In every email we send you'll find original reporting, evidence-based insights, online seminars and readings curated from 100s of sources - all in 5 minutes.

- Twice a week

- More than 20,000 people receive it

- Unsubscribe any time