In this piece

Paying for news: Price-conscious consumers look for value amid cost-of-living crisis

In this piece

1. Introduction | 2. Methodology | 3. Who is paying for online news? | 4. Market context: differences between the US, the UK, and Germany | 5. Motivations for paying for online news | 6. The impact of the cost-of-living crisis on news subscriptions | 7. Price considerations for existing subscribers | 8. How to attract those who are reluctant to pay for news | 9. Conclusions and discussion | Authorship and acknowledgments | FootnotesDOI: 10.60625/risj-x0rq-6c43

1. Introduction

This report uses survey data from 20 countries and qualitative research from the United Kingdom (UK), United States (US), and Germany to explore who is paying for news content online, which publications they pay for, how much they pay, and what motivations they have for subscribing or donating to news.

We focus, in particular, on how the cost-of-living crisis is impacting willingness to pay for online news, through talking to those who have cancelled their subscriptions over the last 12 months as well as those who have maintained subscriptions during this period. We also look at the prospects for attracting new subscribers amid this economic downturn and ask what approaches, if any, might persuade these reluctant consumers to pay for online news in the future. Finally, we use insights from our research to explore ways in which the publishing industry could adapt current strategies around news payment.

Key findings:

- Across most of the 20 countries we analyse, payment for online news is levelling off with high levels of cancellation strongly linked to the cost-of-living crisis.

- Low-price introductory offers are effective at attracting new subscribers but many struggle to see the value when it comes to renewal and paying the full sticker price.

- Long-term news subscribers tend to be male, older, richer, and better educated, with a strong interest in news and politics. Younger subscribers tend to pay less and are more likely to make donations than older groups.

- News subscribers are attracted by a combination of distinctive high-quality, curated, and exclusive content, identification with the brand, a desire to support quality journalism, and a higher-quality user experience.

- Around half of non-subscribers say that nothing could persuade them to pay for online news, but others could be attracted by a lower price, more relevant content, or less cluttered (ad-free) websites and apps.

- For some people the value of news subscriptions is partly conditioned by the amount and quality of free content (from both commercial and public service outlets) available in a market, as well as by the price and experience of entertainment services such as TV, sport, and music.

2. Methodology

We draw on 2023 Reuters Institute Digital News Report surveys from 20 countries where online news payment is widespread (see Figure 1). These surveys, which were conducted by YouGov in January/February 2023, used nationally representative samples of around 2000 people to identify which people pay for news, the most popular providers, motivations for paying and not paying, as well as the proportion that had cancelled in the past year and the reasons for this. We note that asking about payment for online news can sometimes be difficult because of the number of different ways people can pay for or access paid-for online news, such as via a subscription to another type of product or package, through an institution such as a university, or via free or low-cost trials.

Survey data will also not necessarily match industry data, as the latter are often collected and measured in different ways. The benefit of surveys is that we can ask questions about more specific aspects of pay (on cancelling, motivations, etc.) that are not always contained in industry numbers, while also linking this data to different socio-demographic variables. We can also field the same questions to a large number of people across different countries, allowing us to make comparisons across countries and brands, as well as assess payment trends among the broader population (since we survey nationally representative online samples in each country). Detailed survey methodology can be found on the Digital News Report website.1

We supplemented this with qualitative research conducted in the UK, the US, and Germany in February 2023, also by YouGov, where we explored behaviours and motivations in more detail with over 100 participants, over more than a week. We used a qualitative online community, which combined online interviews, prompts, and exercises, allowing us to elicit a deeper understanding of the nature of online news subscription, membership, and donation, as well as pricing and other considerations, from a range of engaged news consumers who i) had maintained a subscription over time, ii) recently taken up a subscription, iii) recently cancelled a subscription, or iv) never subscribed but were potentially interested. The benefit of a multi-day online community is that it allowed participants to provide more detailed and thought-out responses, giving richer insights. The limitation of qualitative data is that they are not representative of the broader population, though we sought a range of participants broadly reflective of each country’s population by age, gender, region, and income/social grade.

Figure 1.

Figure 2.

3. Who is paying for online news?

While the vast majority of news consumers do not currently pay for online news, our Digital News Report surveys have shown there is a significant minority that say they have paid for online news in the last year, either through a digital subscription, combined digital/print subscription, or a one-off payment for an article, app, or e-edition. In some richer Nordic countries, where most publishers charge for at least some of their online news, a third or more have signed up. In the US, a pioneer of digital news business models, around a fifth of our sample (21%) say they have paid. But in many larger European markets where there is a good supply of high-quality free news, such as Germany (11%) and the UK (9%), far fewer are currently paying.

Figure 3.

Over the last decade, the proportion that subscribes or makes a one-off payment or donation to a news organisation has increased from 10% to 17% (average of 20 countries, see Figure 4). Publishers started to charge for online news during a period when journalism was increasingly seen as being under threat. Later, many successful news brands tightened paywalls, or used important news events such as Covid-19 to persuade consumers about the value of reliable information. However, as news subscription reaches a more mature stage, growth seems to have slowed, with publishers struggling to find new customers to replace those that are cancelling.

Figure 4.

Over time, we have also witnessed the type of payments change. In 2014, the vast majority of subscriptions were for print – with digital sold as an added benefit – but today the biggest proportion are ongoing digital subscriptions of different types (46%), with around three in ten (28%) paying for combined print and digital packages. A significant proportion (34%) have a subscription paid for by someone else, for example by a parent or educational institution, or where news is bundled as part of a wider TV, broadband, or mobile deal. Just over one in ten (12%) of those paying say they made a one-off or ongoing donation to a news service in the last year.

Six in ten (60%) of those who make an ongoing payment are men and over three-quarters (79%) have medium to high household incomes. Regular payers also tend to have received more formal education and are more likely to be left leaning politically than right leaning, (especially in the US). Although the majority of those paying are older, this is mainly a reflection of the underlying age distribution in the national populations studied.2 Proportionally, there are no significant differences in willingness to pay across age groups. This finding can perhaps be explained by the fact that younger people are much more likely to have a subscription paid for by someone else or to make a donation,3 which tends to be for a lower amount of money, and by the fact that younger people are still more likely than older people to do just about any online activity.

Figure 5.

Along with education and income, the clearest predictor of online news payment is the level of interest in news and in politics. In the US, for example, eight in ten (79%) of ongoing subscribers or donors say they are very or extremely interested in news and three-quarters (74%) say they are very or extremely interested in politics (compared with 43% and 36% of non-subscribers, respectively). Having said that, only about a third of all those who are interested in news (30%) are currently paying, so there could still be plenty of room for growth with the right product and pricing strategy.

Figure 6.

4. Market context: differences between the US, the UK, and Germany

Willingness to pay for online news is shaped not just by relative interest in news and demographic factors, but also by the wider context. This includes the size of each market, the supply of high-quality free online news, and the tactics and approaches taken by different publishers.

4.1 United States

Paid news content in the US is dominated by upmarket general titles such as the New York Times and the Washington Post, as well as financial titles such as the Wall Street Journal. The New York Times has 9.7m digital and print subscribers and is now selling an ‘all access’ bundle, which includes the Athletic (sports), Wirecutter (reviews), NYT Cooking, and NYT Games. Other brands increasingly find they need to define their offer in a way that complements this category-defining package.

Having said that, the large and entrepreneurial US market supports a range of other paid providers including storied magazines (the New Yorker, the Atlantic), local newspapers, alternative/partisan media (Epoch Times, Blaze TV), niche brands, and specialist newsletters (e.g. facilitated through platforms like Substack). In this mature market, around half (56%) of subscribers say they pay for two or more brands, often a national and local or specialist title in combination. Many brands use hard or metered paywalls with introductory trials (typically $1 or $2 per week) to entice new customers. But with a large number of consumers on lower price offers, average revenue per digital consumer has been falling.4

The US is among the countries with the highest proportion donating to a news organisation in our survey (4% of the US sample), and this includes payments to podcasters and YouTube channels, as well as established brands such as NPR and Vox Media. It is also a market shaped by partisan loyalties, with around half of those paying for news (47%) saying they do so because they identify with certain journalists or the stances of particular brands (see Section 5 iii). Overall, one in five (21%) people pay for online news in the US.

4.2 Germany

The strength of regional and regionally based national titles is a distinguishing feature of the German market. Subscriptions are split between upmarket titles such as Die Welt, Der Spiegel, Stern, Frankfurter Allgemeine Zeitung (FAZ), Die Zeit, Süddeutsche Zeitung, and financial daily Handelsblatt. Local and regional newspapers account for a quarter (25%) of all subscriptions. Unusually, we also find a tabloid newspaper, Bild, as a leader in paid online content. It is one of many publishers in Germany to use a ‘freemium (+)’ model, charging €7.99 per month (or €1.99 for the first year) for exclusive news and entertainment content, packaged with video highlights from the Bundesliga.

BildPLUS has around 675,000 digital subscribers,5 which explains the higher-than-usual proportion of subscribers with lower income/education in our German data, when compared with the US and the UK.6

One other characteristic of the German market is the provision of higher-priced e-editions, which are targeted at former print readers. In some cases, these are bundled with a physical iPad, which is often given away free.7

Strong digital offers by well-funded and highly trusted public broadcasters (ARD, ZDF, and regional alternatives) as well as widely used commercial websites (such as n-TV, t-online, and web.de) means that paid content packages need to offer something deeper or more relevant. Only 11% of people currently pay for online news in Germany.

4.3 United Kingdom

The Times/Sunday Times was one of the first UK publishers to put its content behind a paywall and has amassed around 500,000 digital subscribers over the last 13 years. The Telegraph, a more recent convert to online subscriptions, has achieved similar numbers for its mix of right-leaning political commentary and other specialist content. These two titles account for around four in ten (41%) of all online news payments in the UK. Other popular subscriptions include the Financial Times and The Economist, as well as online versions of weekly political magazines the Spectator and the New Statesman. Most subscribers in the UK pay for only one title.

The Guardian’s pioneering reader contribution model has helped keep its news free to all, while encouraging donations from those who support its left-leaning perspective. In recent years, it has added a digital subscription option for its premium app features such as live content and puzzles. In total, the Guardian has over a million ongoing supporters (with around half of these coming from outside the UK).8

Some other national news outlets (the Independent and iNews) and many local newspapers have recently introduced premium content subscriptions, but with limited success. High-quality free news is widely available in the UK, not just from the BBC, which is the most widely used online provider, but also from commercial broadcasters Sky News and ITV News. Most of the national press continues to be ad-supported, including popular outlets such as MailOnline, the Sun, and the Daily Mirror. These conditions may have made it harder for UK outlets to attract domestic subscribers. Just 9% in the UK have paid for any online news in the last year, but many UK outlets still have high numbers of subscribers by European standards, thanks in part to the broader appeal of English-language coverage elsewhere.

Figure 7. Summary of market context

United States

21% pay

- Upmarket titles dominate, mostly with hard or metered paywalls (e.g. New York Times, Washington Post, Atlantic)

- Tabloids mostly free and local publications starting to charge or ask for donations

- Multiple niche titles at lower price points, including Substack newsletters and Patreon donations

- Over half subscribe to two or more online publications

- Lower average price points and wide use of cheap 12-month trials (e.g. New York Times, Washington Post)

Germany

Germany

11% pay

- Wide mix of upmarket titles and tabloid subscriptions mostly using freemium (+) models

- High incidence of replica e-editions (especially with regional press) targeting older print users

- Subscriptions split across many titles: Bild, Welt, Spiegel, FAZ, SZ, and regional newspapers

- Most people subscribe to just one online publication and donation is rare

- Higher average price points: Digital with replica editions is €30¬40/month, Bild+ is €7.99/month

United Kingdom

9% pay

- Upmarket titles dominate with hard or metered paywalls (e.g. Times, Telegraph, FT)

- Guardian is free to all but with 1m+ contributors via subscription/donation

- Long tail includes political magazines (e.g. Spectator, New Statesman) and partisan outlets

- Tabloid and mid-market remains largely free and very few pay for local titles

- Mixed average price points: Times is £26/month, Telegraph is £25/month, but discounting is widespread

5. Motivations for paying for online news

For those who pay for news, subscriptions play an important part in their lives and their identity. Some subscribers talked about the importance of news in helping them make informed decisions through self-education, as well as fostering a connection with the wider world. Others saw a news subscription as important to their sense of self, shaping their worldview. In Germany, in particular, people spoke of a civic duty to stay informed. Our research suggests that many subscribers go through three distinct phases.

i. Subscription triggers

For many subscribers, interest in and readership of a particular news brand is ‘handed down’ from a family member, often with an affinity with its political outlook or values. This early familiarity often keeps a particular brand front of mind when considering subscription later. Other life-stage changes can also lead to a paid subscription – for example when free student access ends, or when more disposable income becomes available with a promotion at work.

More immediate triggers include frustration with paywalls (as many want to read a specific article or feature they cannot access any other way) or intrusive advertising. A cheap promotional deal often helps push them over the edge.

As we identified earlier, a certain level of interest in news and curiosity about the world is a prerequisite for signing up (and maintaining a news subscription).

ii. Building habits through regular attention

A critical next step is to build paid content into routines. Most publishers pay particular attention to the first 90 days of a new subscriber, pushing them to sign up to newsletters, podcasts, and personalisation features. They know that regular (daily) usage is the biggest predictor of continued subscription. Subscribers acknowledge this too, pointing out how trial periods allow them to ‘get to know’ a brand.

New subscribers nominally trust their subscription, but this is not without reservation. The relationship between new subscribers and their chosen brand can be fragile. Many remain wary of a long-term commitment and are not yet convinced about value.

Cheap offers used to run for a few weeks, but now tend to be much longer (typically a year) to give habits and relationships a chance to develop.

iii. Maintained (loyal) subscribers

In this third stage, subscribers tend to have integrated paid content into their routines and have developed a high degree of loyalty. Maintained subscribers feel that their subscription represents high-quality, truthful journalism, often framed in opposition to other brands. They often feel that their chosen outlet, in their view, speaks to them and for them – they use the brand as a shortcut for ‘what to believe’, particularly in the US and the UK.

This older subscriber sums up the journey she has been through across different life stages, from indifference to deep attachment:

While the stages of awareness, habit-building, and loyalty are common across countries, the specific drivers can vary, most likely linked to market context. In the US, where concern about misinformation, bias, and clickbait tends to be high,9 getting access to higher-quality content (65%) is the biggest motivation among subscribers for taking out a subscription (see Figure 8). And in Germany, where a range of news is easily accessible from public broadcasters, a key distinguishing feature of paid news is its greater perceived depth.

Americans are also more likely to cite ‘funding good journalism’ as a reason (38%) for subscribing, compared with Germany (30%) and the UK (29%), perhaps because consumers in the latter two markets feel they have in some sense already contributed via fees to public broadcasters.

Figure 8.

Many of those in the US who say they want to support good journalism self-identify with the left, where many feel that their political beliefs and values are threatened.

This perhaps explains why US publications are more likely to stress their mission and values in marketing messaging such as ‘Truth Matters’ from the New York Times and ‘Democracy Dies in Darkness’ from the Washington Post. Other studies have found that this type of ‘normative’ messaging tends to be most effective in combination with other factors, such as low-price offers.10 We also find that, when it comes to paid subscriptions, identification with specific journalists and news brands is especially important in the UK and the US, where the political positioning of a brand is an important part of the value proposition.

By comparison, traditional brands in Germany often take a more neutral position, appealing to a bigger pool of readers from both left and right. German subscribers say they are motivated by price factors (29% cite being offered a good deal or trial as a reason for paying, compared with 22% in the UK), as well as the quality of content.

Other less central, but still important, motivators behind subscriptions include games and puzzles or coverage of lifestyle topics such as film, travel, fashion, or food. These ‘softer’ non-news features are especially good for maintaining subscriptions – but less of a reason to sign up in the first place.

Finally, ease of use of a website or app is highly valued. Fast-loading pages, well-organised content, and low ad density are often mentioned by consumers as key benefits of a paid subscription. In fact, an ad-free experience is the base-level expectation that many subscribers (and potential subscribers alike) have of news websites and apps.

Overall, we find a combination of five factors motivating news subscribers. These are (i) distinctive and high-quality news and analysis, (ii) alignment with the values or political outlook of the brand, (iii) a desire to support good journalism, (iv) a premium user experience, and (v) lifestyle features, puzzles, and games. The appeal of each element partly depends on the market, including the quality and range of available free content. Beyond that, certain triggers such as cheap offers can be used to entice new subscribers, but they are unlikely to maintain their payment unless other conditions are satisfied. New subscriptions can be precarious, as we outline in the following sections.

6. The impact of the cost-of-living crisis on news subscriptions

Our 2023 Digital News Report survey finds that, across 20 countries, at least a third of subscribers cancelled or renegotiated the price of their subscription between January 2022 and January 2023. Analysis of open-ended responses showed that the cost of living was by far the biggest reason for cancellation, along with a perceived lack of regular use. The chart below suggests that while around half of subscribers are happy with their subscription, the other half are much less committed.

Figure 9.

Our interviews with 30 lapsed subscribers in three countries help bring these datapoints to life by exploring how the squeeze on household spending has affected consumer thinking. For many, the downturn has led people to look at their costs in forensic detail, just to make ends meet or because they were looking to save money for a substantial purchase such as a car or holiday. Users often engaged in a cost–benefit analysis, weighing the price and value of a paid news subscription against other regular outgoings.

For some in the UK, a key trigger point was the end of a low-price trial – especially in the face of potentially sharp increases to full-price subscriptions, a leap many were unwilling to make. For others, it was a change in life circumstances.

In the US, where the impact of energy price hikes and inflation has been less severe, there were fewer direct mentions of the cost of living. But the high price of news subscriptions (especially after trials ended), compared with the perceived value that people felt they were getting, was a regular theme. People were conscious if they hadn’t used their subscription enough for it to feel ‘worth it’.

Beyond cost, we did find some other factors at play in the US, including dissatisfaction with the brand’s political views or a specific editorial decision. Many subscription-based publications are struggling to balance a commitment to objectivity and balance with the expectations of their politically committed readers. This has become a particular problem in commentary sections, with liberal subscribers often objecting to views that challenge their own:

On the New York Times

On the New York Times

A large number of people were reported to have cancelled their New York Times subscription following a commentary piece several years ago by a US senator calling for a military response to civic unrest in American cities.11 These tensions remain at the heart of reader-first business models, which lean towards pleasing (or at least not antagonising) a specific group of highly politically committed readers.

7. Price considerations for existing subscribers

One of the biggest surprises in our research is the markedly different prices being paid for the same product. It is understandable that new subscribers may pay less than loyal ones, as they tend to be on introductory offers, but we also found that many maintained subscribers were paying a price much lower than the one advertised.

Our research suggests that consumers have become increasingly conditioned to expect special offers. These introductory prices are highly effective at attracting users in the first place, but often hard to wean consumers off when the renewal comes around:

On the New York Times

On the New York Times

This jump from a trial price to the full sticker price has become a key challenge for publishers, compounding the problem of churn as subscriber bases have grown. This is because more new subscribers are now required each month to make up for those leaving. Part of the response by some publishers has been to lengthen the trial period to give more opportunity to build those critical habits. And for some, this seems to be working:

On the Wall Street Journal

On the Wall Street Journal

But this still leaves the problem of the renewal price with this young person, who is on a medium to low income, prepared to pay ‘a more reasonable $5/month’ – still a far cry from the full-price ticket of around $39/month.

To address this gap, some publishers have started to experiment with differential pricing at the point of renewal to better match price to perceived value. Other publishers are experimenting with stepped pricing or have offered special deals to younger consumers.

How news stacks up against TV streaming and other subscriptions

Our previous research has shown how the majority of consumers, especially younger ones, have one or more ongoing TV streaming subscriptions, and often a music or sports subscription as well.12 Widespread adoption of online entertainment subscriptions such as Netflix and Spotify have almost certainly made it easier for publishers to charge for online news, by conditioning user expectations.13 Publishers have also been able to learn from successful acquisition tactics by streaming services such as low-cost trials.

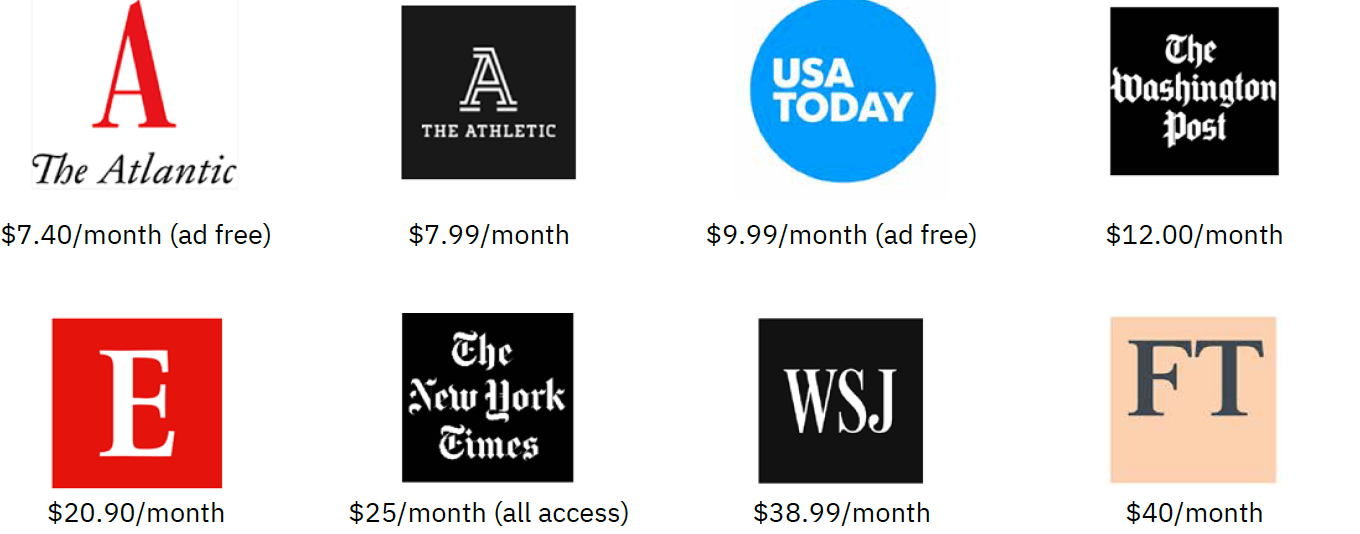

In addition, entertainment pricing has also often been used as a reference price by news publishers. In Germany, for example, the monthly subscription for Bild PLUS, €7.99, is the same as the price Netflix charged there until recently. USA Today charges $9.99 for its no-ads digital access – the same as Netflix’s basic no-ads tier, though this has recently substantially increased.

While some publishers may be relatively happy with a price that is similar to streaming services, many premium news brands would like to charge considerably more. Many already do (see below).

Figure 10. Selected monthly standard subscription prices – US

Entertainment

Entertainment

News

Our interviews for this report suggest that many consumers do still look at online subscriptions ‘in the round’ for budgeting purposes. In the following case, a young woman in the US, when reviewing monthly outgoings, decided to keep all her entertainment subscriptions but ditch the Washington Post.

When making a decision about subscriptions, the price of each subscription was often a factor, along with how many members of the family benefitted. News subscriptions sometimes compare unfavourably because they tend to be valuable to just one person in the household.

Research participants also commented on the emotional benefits of entertainment subscriptions (diversion, fun) and contrasted this with the often negative and downbeat nature of news consumption (often seen as more of a duty or chore).

But this was not a universal view. Even if TV streaming subscriptions influence expectations around price, many consumers place news and entertainment in different categories, both equally important but playing different roles in their lives.

Our sample is not large enough to come to definitive conclusions, but the role played by reference pricing from streaming services seems to be more important when it comes to younger subscribers. Some older consumers appeared to be more influenced by the price of offline services they had paid for in the past, such as a print subscription. In that context, an online news subscription can often feel like a bargain.

Our interviews suggest that people of different generations may have different expectations about price based on reference points that are meaningful to them.

Critically they also suggest that ability to pay differs across generations, life stages, and income levels – with most current pricing strategies struggling to accommodate these factors.

To address these issues, some publishers have started to develop a wider range of products at different price points. These include more expensive replica editions for older users and cheaper ‘cut down’ versions for younger audiences (see below).

Different news products may be one way to go

An alternative strategy is to deploy differential pricing for the same product at the point of sign-up. Der Spiegel, for example, has a cheaper offer for under 30s and for families. Other publishers have started to experiment with differential pricing at renewal, based on factors such as previous usage or age.14 Either or both of these tactics may help to manage expectation gaps around value identified here, but they do raise issues of equity and fairness.

The feeling of being ‘limited’ by a news subscription

One of the more unexpected findings to come out of our research was the notion of news subscribers feeling ‘limited’ by their subscription to a particular brand. Those who had cancelled subscriptions talked about feeling restricted to a single source.

This was, in many ways, connected to a sense that they had to make frequent use of the subscription for it to seem worth it. The time required to consume content from one brand, some expressed, bound them to that outlet and limited the time they had to consume news from other sources, thus limiting their perspective.

For some who had cancelled their subscription, there was a feeling that their experience was now better because they felt able to look at multiple sources and understand different perspectives on a topic. Many non-subscribers appreciated the diversity of the multiple free sources they had access to.

For others, however, there was a feeling that they were worse off after cancelling. This was, they said, because the free news available to them lacked the depth or insight of the content in their subscription. They also had to spend more time visiting different news sites to get the information they wanted. A subscription can help cut through the noise by providing a curated experience.

The notion of feeling ‘limited’ by a subscription to a single news brand points to the potential value in bundles. Services like Apple News+ have proven popular, particularly among younger people, because they offer access to more than one title.

8. How to attract those who are reluctant to pay for news

We have been focusing so far in this report on current or recently lapsed subscribers or donors. But it is worth remembering that, averaged across the 20 relevant countries in the 2023 Digital News Report, the vast majority (83%) are not currently paying for news.

Focusing on the US, the UK, and Germany, we find that half or more of those who are not currently paying say nothing could persuade them (65% in the UK, 54% in Germany, and 49% in the US). However, this still leaves a considerable number who might be enticed by a lower price, more relevant content, or a better user experience.

Of these, our survey suggests that the factor that would make the biggest difference is price – (i) a lower, more affordable package, (ii) the ability to share the cost of subscriptions among friends and family, or (iii) a subscription that includes more value (some kind of bundle). Taken together, these options appeal to three in ten (29%) non-payers in the US and around a fifth in Germany (22%) and the UK (20%).

Figure 11.

Not surprisingly, the issue of price resonates most with younger users, who are mostly being asked to pay the same amount as older groups for a product whose content does not feel relevant to them, while also having less disposable income.

Figure 12.

In order to be enticed to pay, non-subscribers felt like content had to be exclusive, curated, and, crucially, unavailable for free. They asked: Why pay for news when I can access the same breaking news and current affairs stories for free elsewhere?

In previous research we found that the availability of free sources was the biggest reason given for not paying for news.15 Many non-subscribers felt that subscription offers were not unique or valuable enough to them as individuals. Subscriptions needed to offer them something more. A ‘free news mentality’ can be tough to break through, as many who have been able to freely access news online for years don’t see why they should now be asked to pay.

Another factor putting people off subscribing, especially with younger users, was a sense that signing up to a paid content source would limit the time they had to pick and choose more diverse sources (as noted in Chapter 7). This is a core part of how young people, in particular, like to consume news, which is why bundled offers like Apple News+ often appeal to these groups. Among subscribers in the US, almost a third (29%) of those under 35 are subscribed to Apple News+, while only 13% of those over 35 are similarly subscribed.

Potential subscribers were aware of cheaper introductory offers, but they were wary about being caught up with a long-term commitment – and paying money for something that they did not end up using. A related barrier, felt particularly strongly in Germany, was a difficulty in cancelling.

This frustration – and the converse appeal of an easy-to-cancel subscription – was also mentioned elsewhere. The ability to cancel any time, particularly without having to pick up the phone, was appealing to many in the UK.

Overall, potential subscribers were split as to the value of a subscription. Some felt a subscription might encourage them to read more and hence ‘enhance’ their news consumption, others that it could reduce the diversity of their news consumption. Some potential subscribers were attracted by specific columnists or articles they could not read for free, but many said that they had not found the right source to fit their wants or needs.

Key barriers in summary

- The price of subscription, including value for money when compared with free sources.

- The time required to take ‘full advantage’ of their subscription.

- Relying on a single source of information and not having a ‘rounded view’ on different topics.

9. Conclusions and discussion

Our research shows that, averaged across 20 countries, less than a fifth (17%) are currently paying for online news. This group tends to be male, richer, and better educated, with a strong interest in news and politics. Most of those paying full-price ongoing subscriptions are older, while young people tend to pay less or not at all.

Subscribers are motivated by a desire to access higher-quality news than is available from free sources. They are also looking for a premium user experience or additional benefits such as lifestyle features and games. In some countries, including the US, a desire to support ‘independent’ journalism is a critical factor, as is identification with the values or political outlook of the news brand.

Maintained (loyal) subscribers tend to use content every day and have developed a deep connection with the news organisation and its journalists. Over time, they become comfortable with the price they are being asked to pay, develop a strong level of trust, and use the brand as a shortcut for ‘what to believe’.

But our research has also identified a large number of subscribers who are much less committed, either because of the cost, or because they are not yet using the service regularly enough. Amongst lapsed subscribers many were enticed by low-price introductory offers, but baulk at the cost when renewal comes around and compare their subscription, often unfavourably, with other ways of spending their money.

The cost-of-living crisis may have accelerated these trends, with around four in ten subscribers saying they tried to negotiate a better deal or have cancelled their payment in the last year because they can no longer afford it.

Looking through a glass-half-full lens, however, we note that, despite the downturn, the overall number of subscribers has not fallen, and many news publications continue to grow, albeit slowly, despite the difficult economic conditions. We have also identified in this report a very large number of potential subscribers with a high interest in news and strong brand connections who are actively looking for higher-quality or more relevant sources of information. The key problem here is a mismatch between the price they are being asked to pay and what they think a news subscription is worth.

If publishers could find a way to charge on the basis of perceived value, many more people could become subscribers over time. Publishers recognise this affordability gap and are developing responses. In Germany, many brands are offering lower-price subscriptions for students or younger people, while the Guardian’s contribution model in the UK allows people to pay what they can afford. In the US, publishers are offering longer introductory trials in the hope of proving value and considering differential pricing as a way of varying the price at renewal.

But even if the ‘price puzzle’ can be solved, there is a more fundamental challenge. Some people who are interested in news do not want to be tied to or ‘limited’ by one source, and most of them are not prepared to pay for multiple news subscriptions. Our research shows that both existing and potential subscribers are drawn to the idea of all access bundles that combine multiple titles, podcasts, and other benefits. This helps to solve the value problem and, as the New York Times has shown, dramatically reduces the rates of churn. Once again, the stumbling block is price, with people prepared to pay a little more for their news but possibly not as much as publishers would like.

The decline in referrals from Facebook and Twitter (now X) and uncertainty over search traffic in the era of AI-powered chatbots have increased the urgency of making paid online news work. This research has highlighted the barriers that need to be overcome, as well as the many opportunities that exist to reach new subscribers. If the price is right and the value can be clearly shown, the future of journalism can still be bright.

Authorship and acknowledgments

Nic Newman is Senior Research Associate at the Reuters Institute for the Study of Journalism and is also a consultant on digital media, working actively with news companies on product, audience, and business strategies for digital transition. He writes an annual report for the Institute on future media and technology trends.

Dr Craig T. Robertson is a postdoctoral research fellow at the Reuters Institute for the Study of Journalism whose interests include trends in news consumption, audience trust in and perceptions of news, and the impacts of technology on the news industry.

The authors would like to thank the team of qualitative researchers at YouGov for their work with the online community on the topic of news payment, in particular Mariana Owen, Jerry Latter, and Charlotte Clifford. Also, thanks to Richard Fletcher, Director of Research, for his helpful suggestions on improvements to the text and for his additional insights.

Published by the Reuters Institute for the Study of Journalism with the support of the Google News Initiative.

Footnotes

2 41% of people surveyed across the 20 markets are in the 55+ age bracket, with the other 59% spread across younger age brackets.

3 17% of payers under 35 made a donation in the last year, compared with 10% of those aged 35+. Also, 23% of payers under 35 had subscription paid for by someone else in the last year, compared with 13% of those 35+.

6 In Germany, 20% of ongoing subscribers are on low incomes and 21% have lower education, compared with 18% and 12%, respectively, in the UK, and 16% and 6%, respectively, in the US.

9 Bias, Bullshit and Lies: Audience Perspectives on Low Trust in Media. Reuters Institute. 2017.

10 ‘Subscribe Now: On the Effectiveness of Advertising Messages in Promoting Newspapers’ Online Subscriptions’.

13 Fletcher, R. and Nielsen, R. K. 2020. ‘Are Netflix and Spotify Subscribers More Likely to Pay for Online News? Comparative Analysis of Data From Six Countries’, International Journal of Communication 14.

15 55% of non-payers in the UK, 53% in the US, and 40% in Germany cited this as a reason not to take up paid news. Digital News Report 2017.

This report can be reproduced under the Creative Commons licence CC BY.

More on: